by Stephen Malpezzi, Professor and Lorin and Marjorie Tiefenthaler Distinguished Chair in Real EstateOne of the goals of my

urban economics classes is to demonstrate how we can use economics, and data analysis, to understand a range of events in real estate markets, in cities, and in our society more broadly.

Tomorrow's midterm election provides us with a great set of teachable moments. I'm using the effect the economy can have on the election to illustrate some basic techniques of data analysis, critical thinking, and "storytelling;" and, as always, how "

Reading for Life" can help us make sense of the world.

Today, I'd like to share just a few of these points, focusing less on the data analysis techniques and more on some interesting stylized facts and research results (mainly results from other people's research).

While much debate surrounds causes, timing, and attribution, the objective fact is that, by some measures, the economy is in the worst shape since the Depression. The next two figures show how two indicators, growth in GDP per capita and inflation, fared during the terms of the postwar presidents since Truman. (The data go back to 1947 and so the early part of Truman's term is omitted. The data run through Q2 of 2010, so the last few months of the Obama administration are also omitted). Let me start with two indicators that previous research has tied to electoral performance.

FIGURE 1. President Obama, so far, has faced a lower growth rate of GDP per capita than any other postwar president. Of course, it's early days, and whatever our partisan leanings, we all hope for better performance in the next two years. Nevertheless, the anemic performance of GDP growth is a challenge for Democrats (who, of course, also control the House and the Senate, at least by the simple definitions of "control.")

FIGURE 2. On the other hand, Obama has held office during a period that's exhibited lower average inflation than we've seen during any other postwar President's term.

Are Presidents responsible for “their” economic averages?A huge body of research argues the effects of economic policies (taxes, subsidies, deficits, regulations…) and Presidents (and other politicians) do affect these policies. However, the economy has a lot of inertia (lags) built in, and there is a lot of luck involved. (Luck, of course, can be good or bad.) Policies have their lags, too. The economy can react to the perception of future policies and uncertainty in the same. But fair, or not, there is a lot of evidence that election outcomes are affected by the performance of the economy, even over short periods.

Economist

Ray Fair (Yale) has published several papers and a

book about how to forecast U.S. elections according to the state of the economy. Recently he extended his work from Presidential elections (as in his book) to House elections, in “Presidential and Congressional Vote-Share Equations,”

American Journal of Political Science, 53(1), January 2009, pp. 55-72

Ray Fair’s prediction of this week’s Congressional electionFair’s model has three equations: for the Presidential vote, the “on-term” House vote, and the midterm House vote. The economic variables are derived mainly from growth in GDP per capita and inflation. Other variables include whether there is a Presidential election, and if there’s a war on.

Fair’s latest forecast (10/29/10) is that the Democratic share of the House vote will be 49.2%, i.e. a razor-thin Republican majority. He doesn’t forecast Senate results.

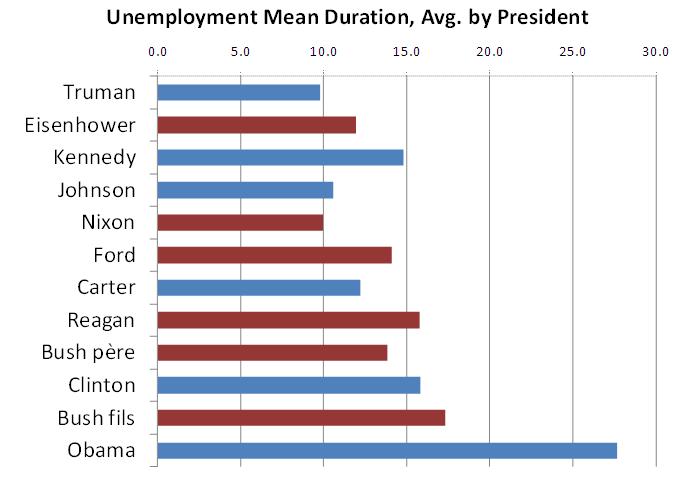

What about unemployment?Fair’s model shows the House vote as closer than most political pundits. The two main economic drivers in his model are GDP per capita growth and inflation. Current low inflation numbers are helping to keep it close. I think the other thing this model misses is our high unemployment and its extraordinary average duration. See the next two figures:

These are even worse than might be expected from our recent growth in GDP; see for example the

analysis by the Federal Reserve Bank of San Francisco. High unemployment, and high duration, and how they are now driving foreclosures, are subjects my colleagues and I have discussed

elsewhere.

Debate will continue on the efficacy of the policies of the Administration and Congress; between Republicans and Democrats; and the debate that’s always on within the parties.

Despite my PhD in economics, I’d never argue that elections are only about my favorite subject.

But objective data, and past research on elections, show that the state of the economy has an important effect on the electoral fortunes of the party in power. Fairly or not, economic conditions favor the Republicans this time around.

More "Reading for Life"- Fair, Ray C. Predicting Presidential Elections, and Other Things. Stanford University Press, 2002.

- Gelman, Andrew. Red State, Blue State, Rich State, Poor State. Princeton University Press, 2008.

- Tim Besley's 2002 Lindahl Lecture, Principled Agents.

- William Easterly, Michael Kremerb, Lant Pritch and Lawrence Summers, Good policy or good luck? Country growth performance and temporary shocks. Journal of Monetary Economics, 32(3) December 1993, pp. 459-483.